2025 FCF & Dividend List

Continuing the tradition!

This tradition started at the old blogger site 8percentpa.blogspot.com but it seemed that many readers like it, so we shall continue here. We have past lists going back decades!

This year instead of using Poems, we will try out a new platform - Finchat.io. This is one of the most powerful toolkit for publicly listed stock research and I would encourage all readers to give it a try. It's a freemium model, so anyone can use the free ones, which is already very powderful!

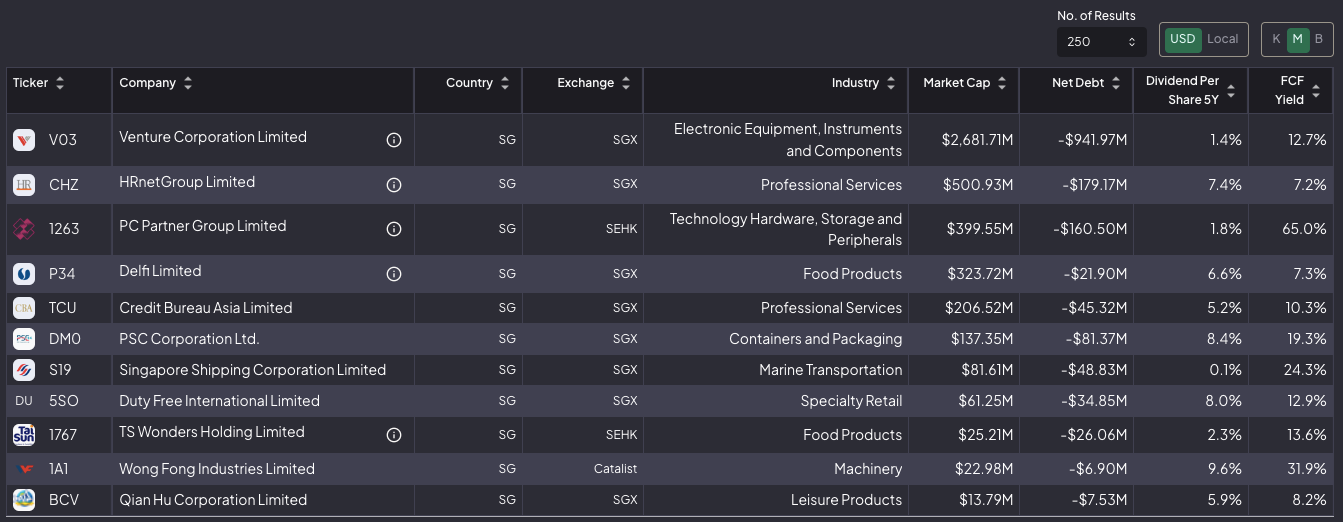

For this year's lists I have similarly used FCF as the main filter, but added dividend and net cash and excluded certain industries. Here's the list for Singapore:

Venture (Market cap c.SGD3.6bn) is the stand out here, with 35% of its market cap in cash and generating a whopping 12.7% free cashflow yield. This stock used to be a darling with share price hitting >$25 a couple of times since its IPO (today's share price is $12.5). It competes in a very good niche today, making hardware for the leading players in life sciences and networking equipment, the growth segments of today. The firm have successfully transitioned from making PC and printers eons ago with its decades of know-how.

However, such hardware manufacturing business is inherently cyclical and share price had gone through many boom and bust cycles. Today, it is trading near trough valuations but without studying closer, it is hard to say when things would recover. It is also worth noting that the founder still runs the company and Venture's success over the last 40 years is largely attributable to him. Should he retire, it is unclear if the company can continue to grow and compound as it had.

This second list churns out the US names of which Acuity (AYI, Mkt Cap USD8.7bn) and Dolby(DLB, Mkt Cap USD7.8bn) are the largest. Acuity makes lighting and Dolby makes sound systems. In this substack, we have covered IMAX, which is in the same space as Dolby - cinemas. Both names look interesting but again, without doing the work, it is hard to say if they are good buys are not. The other issue with US stocks for us is also withholding taxes. Dividends get taxed at 20% and so it makes more sense to buy US stocks with little dividend if we really want to optimize returns. Alas, almost all the stocks on this lists all have very high dividends (after it’s a dividend list). Dolby has a whopping 9% dividend! Maybe it’s ok to give a bit back to the US government, so they can stop bitching about spending too much in Ukraine.

Given the craze on Japan in 2024 and hopefully we see more buzz in 2025, this last list is on Japanese names. For those of us who don't look closely at the land of the rising sun, Japan has been undergoing a stealth transformation for many years after the burst of its bubble, banking crisis and corporate governance overhaul. The stock market finally exceeded its high in 1989 and a huge wave of shareholder activism is under way. We might see Nikkei successfully breaking through at hit 45,000, if not 50,000.

This is not a number plugged out of thin air. The math around it is as follows:

Next year's Topix EPS (2026) is c.220 yen (and growing) and multiplying that by PER of 16x (one turn higher than its historical average to reflect Japan's transformation discussed above), we can explain Topix at 3,520 (vs only 2,800) today.

The Nikkei / Topix ratio has a historical average of 14x and using that (i.e. 3,520 x 14), we have Nikkei at 49,280.

With that, 50,000 is not too far away. Permutations with the no.s above will give you 45,000 to 50,000.

Although we do need the yen to remain weak and the activism momentum to continue. Japan has had so many false starts over the decades it is hard to believe whether the country could really embrace capital markets transformation. I think Japan can change and will change because this provides part of the solution to solve its aging issue (e.g. higher returns to fund healthcare and also more capital to attract workers into Japan).

Besides, Japanese themselves are frustrated that countries that were behind (China and Korea) are now richer. This is a strong impetus to push the country to progress. As with most Asians, Japanese hate “losing face”. With that, we shall discuss two names on the list briefly. Both have what Japan is most famous for: animation:

Bandai Namco (Mkt cap USD22bn, net cash at c.USD2.5bn, dividend yield 4.5%, FCF yield 5.7%) is the ultimately anime IP play with its strong library of the most famous IP and manga titles like Dragonball, Naruto, Gundam and One Piece. Its businesses span toys, games, amusement centres but as with most sleepy Japanese management, financial metrics such as OPMs and ROEs are not optimized and hence we see the stock trading cheaply. Activists need to come in to shake things up.

Nippon TV (Mkt cap USD4.8bn, net cash USD1bn, dividend yield 1.1%, FCF yield 5.5%): broadcasters are right in the middle of shareholder activism with Fuji TV being targeted. The other four broadcasters including Nippon TV all face similar issues with Fuji TV: declining core business, too many headcounts and too many favors paid to star producers and actors and traditional management who knows nothing about capital markets and doesn't give a shit about shareholders. Hence, they all trade below book despite owning some of the most valuable properties on prime land in Tokyo. Nippon TV also owns the crown jewel of Japanese animation - Studio Ghibli (above). As such, there is a lot of hidden value beneath the PBR <1x apparent cheapness. Just need to dig more!

So, hope these ideas help but please conduct your own deep dive research. Our substack will also write these out should they qualify to be in the portfolio.

Huat Ah!

This post does not constitute investment advice and should not be deemed to be an offer to buy or sell or a solicitation of an offer to buy or sell any securities or other financial instruments.