Investment Idea #10 - Live Nation

Net Income vs Free Cashflow, which is more important?

This company is not our typical strong financials, high ROE and high margin company. Its net income is barely positive and this makes the Price Earnings Ratio (PER) and Return on Equity (ROE) numbers look erratic. But FCF generation is strong and growing which makes the stock worth looking at. Again, let’s start with the financials.

Simple financials (Dec 2023 estimate, USD)

Sales: 19.1bn

EBITDA: 1.7bn

Net income: 0.2bn

FCF: 1.0bn

Debt: 4.9bn, Mkt Cap 20.4bn

Financial Ratios

ROIC: 8.0% (Company intentionally keep NI low…)

EV/EBITDA 11.7x (Dec 24)

PER 78.5x (Dec 24)

Past margins: OPM 5%

FCF yield: mid to high single digit for last few years

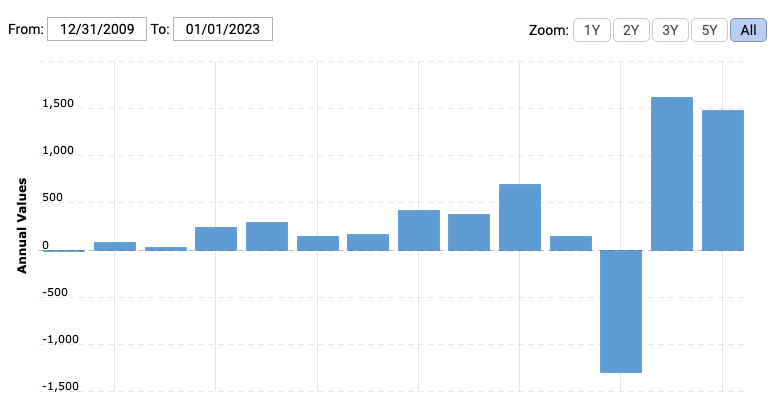

Before 2009, the company was generating negative FCF as it just started building its moat and it only started generating three digit million FCF from around 2012. But when the pandemic hit in 2020, FCF turned hugely negative to -USD1.3bn but has since recovered strongly. Analysts expect FCF to be USD1-2bn in the next 3 years.

Keep reading with a 7-day free trial

Subscribe to 8% Value Investhink to keep reading this post and get 7 days of free access to the full post archives.